RBI’s Open Market Operations (OMOs), often described as a simple liquidity tool, took on a much bigger role in FY26: against the Centre’s gross borrowing of about ₹14.6 lakh crore, RBI’s OMO purchases absorbed a large part of the supply, helping keep bond market conditions orderly and yields from rising too sharply. This note explains how OMOs work, reviews RBI’s 10-year OMO history, and then focuses on FY26 to show why the line between liquidity management and indirect fiscal support has become so important for treasury investors.

Introduction

Open Market Operations (OMOs) are one of the RBI’s main tools to manage liquidity in the banking system and interest rates in the economy. In recent years, however, OMO purchases have also quietly helped absorb a large chunk of the Centre’s bond supply, which has led the market to argue that RBI is, in effect, “funding” the fiscal deficit to some extent.

This primer explains:

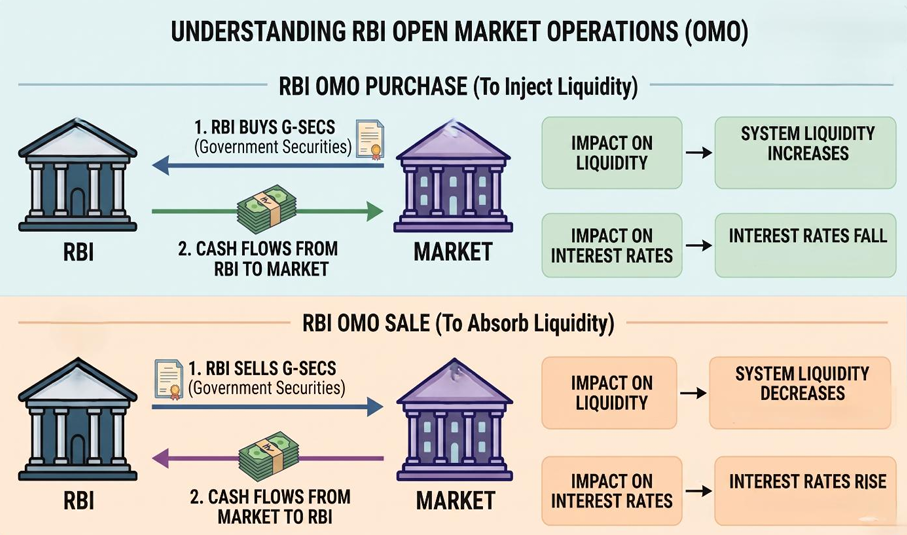

What are RBI’s Open Market Operations?

In simple terms, Open Market Operations (OMO) are when the RBI buys or sells government securities (G‑Secs) in the secondary market.

Source: RBI, HDFC Tru

RBI carries out OMOs mainly to:

OMO is technically a monetary‑policy / liquidity tool, not a budgeted fiscal‑financing route, but the effect on bond markets can look like direct support for government borrowing.

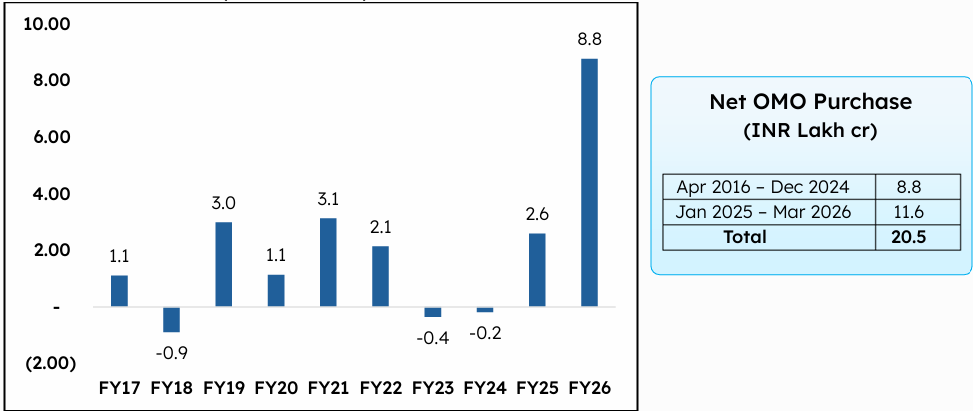

OMOs in the last 10 years – key trends

Over the last 10 years, RBI has used OMOs in different ways, depending on the macro and fiscal backdrop.

Net OMO Purchase (INR Lakh cr)

Source: RBI, HDFC Tru; Note – positive value denotes OMO purchase and vice-versa

FY26 OMO vs Central Government borrowing

In FY26, the Centre’s gross borrowing through issuance of government securities was very high. OMO purchases of INR 8.8 lakh cr accounted for 60% of Centre’s gross market borrowing and 82% of net borrowings in FY26.

![]()

Source: RBI, HDFC Tru

This had two important effects on the bond market:

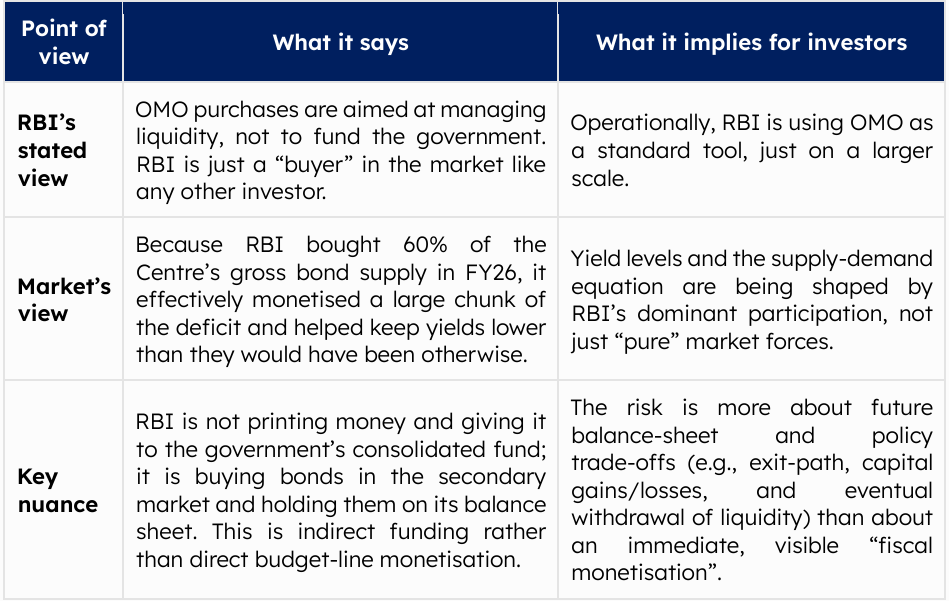

How to read the “fiscal funding” argument

Market participants including economists often say that RBI’s OMO purchases in FY26 were effectively a form of fiscal financing, even though RBI officially calls OMO a liquidity‑management tool. Here’s how to think about this nuance:

Practical takeaway for fixed income investors

For treasuries and large investors, there are three key messages from this OMO story:

Our take:

With budgeted gross central government borrowing elevated at around INR 16 lakh cr in FY27, we expect the RBI to retain a bias toward OMO purchases to smoothen the large supply calendar and support orderly absorption of government securities. While OMOs are officially a liquidity tool, recent experience shows that they can also help the market digest heavy sovereign supply and prevent an abrupt rise in yields.

2024 HDFC TRU

2024 HDFC TRU