The INR has depreciated by around 8% since the start of 2025 to ₹93/$, emerging as Asia’s worst-performing major currency since 2025, driven by ~$38 billion in FPI outflows, US tariffs and a widening current account deficit (CAD). The RBI responded aggressively intervening across both the spot and NDF markets, and imposing restrictions on offshore NDF positions in April-26, but volatility persists. With the INR’s trade weighted REER now at around 94, currency instability remains the primary barrier to FII re-engagement, and a durable recovery hinges on a sustained exchange rate stability.

Executive Summary

Over the past 15 months, the Indian Rupee (INR) has undergone one of its most significant depreciation episodes in recent memory. After a remarkably stable two-year phase between Jan’ 2023 and Dec’ 2024, during which the currency depreciated only ~3.5% in absolute terms (far below regional peers), the INR entered 2025 in freefall.

The Indian Rupee (INR) depreciated from ~₹86 in early 2025 to ₹93 by April 2026, making it Asia’s worst-performing major currency since 2025. The weakness in INR has been driven by a mix of record FDI outflows, US tariff shock and a widening current as well as capital account deficit.

What Drove the Decline?

The RBI has responded with a multi-pronged intervention strategy spanning spot markets, NDFs, forward books, and regulatory reforms. Despite this, INR remains under pressure, and its instability continues to be a principal deterrent to FII re-engagement.

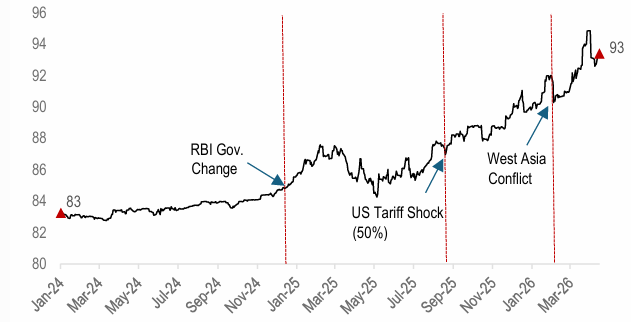

The 52-week range of USD/INR has spanned from ₹84 to ₹95, a swing of over 13%. As of April 2026, the rate hovers around ₹93/$, reflecting a year-on-year change of ~9%. This note examines the forces behind the slide, the RBI’s response, and what it means for foreign investors.

Figure 1: USD/INR Exchange Rate

Source: Bloomberg, HDFC TRU. Note: Priced as of 15th April 2026.

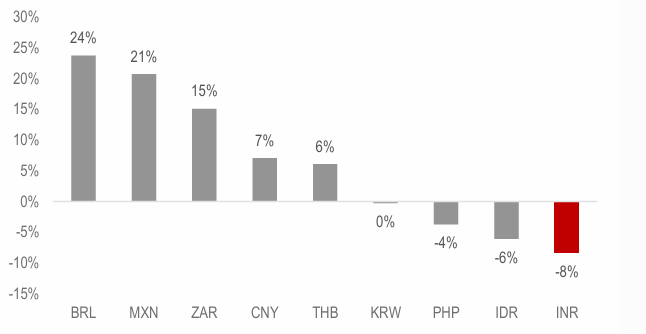

INR Among Global Peers: Asia’s Weakest Link

The INR’s underperformance since 2025 was not merely relative to the US$, it stood out even against other beleaguered emerging market currencies. Driven by a uniquely adverse combination of US tariff exposure, persistent capital outflows, and a record trade deficit, the INR depreciated approximately 5%/4% against the US$ in CY2025/2026 YTD, making it Asia’s worst-performing major currency and one of the weakest among broad EM peers.

Figure 2: EM Currency Performance vs USD (Jan 2025 – April 2026 MTD)

Source: Bloomberg, HDFC TRU. Note: Priced as of 15th April 2026.

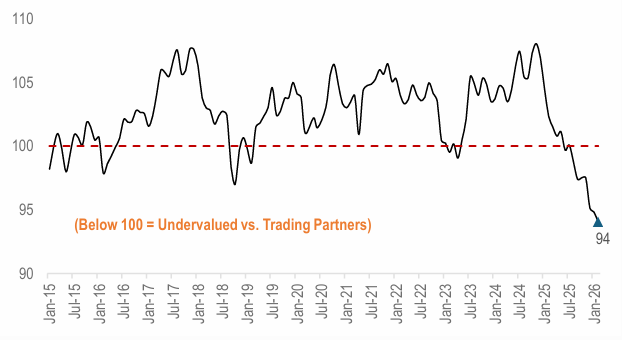

Real Effective Exchange Rate (REER): From Overvalued to Undervalued

The Real Effective Exchange Rate (REER) which adjusts the nominal exchange rate for inflation differentials versus trading partners provides the most important signal of underlying currency valuation. For most of the past decade, the INR’s REER hovered above 100 (its fair-value baseline), indicating an overvalued rupee.

The REER peaked at approximately 108 in late 2024 before sliding below 100 in mid-2025 and further to ~94 by early 2026. This represents a meaningful swing in India’s competitive position.

Figure 3: India’s 40-currency trade-weighted REER at its lowest level since 2015

Source: Bloomberg, HDFC TRU. Note: Priced as of 15th April 2026.

What is a Non-Deliverable Forward (NDF) ?

A Non-Deliverable Forward (NDF) is an over-the-counter (OTC) currency derivative that allows market participants to hedge or gain exposure to a currency, such as the INR, without requiring physical delivery of that currency. Settlement occurs in a freely convertible currency (typically USD), based solely on the net difference between the contracted NDF rate and the prevailing spot fixing rate at maturity.

A Simple Example:

Suppose a US-based investor expects to receive INR 10m in six months but fears the INR will lose value against the USD. To hedge this risk, they enter into a Non-Deliverable Forward (NDF) with a bank at a contracted “forward rate” of 90.0 INR/USD. Six months later, if the market “spot rate” has shifted to 91.0 INR/USD (meaning the Rupee weakened), the bank calculates the difference between the 90.0 contract and the 91.0 market price. Instead of trading the full INR 10m, the bank simply pays the investor the loss in value, which is approximately $1,220, settled entirely in US$. This cash settlement compensates the investor for the INR’s decline without either party ever having to deal with local Indian banking regulations or physical currency delivery.

Why the Offshore NDF Market Matters:

The offshore USD/INR NDF market is one of the most liquid EM currency derivative venues globally, with average daily turnover estimated at $40–50 billion, considerably exceeding the onshore forward market. Sentiment and pricing in the NDF market can transmit directly to onshore spot and forward rates, creating a channel through which offshore speculative pressure amplifies domestic INR moves. This linkage is the primary reason the RBI has increasingly turned to NDF market regulation as a policy lever.

The RBI’s Policy Response to INR Volatility

The Reserve Bank of India (RBI) has recently navigated a period of intense currency pressure, as the Indian Rupee (INR) hit historic lows, crossing the ₹95/$ mark in March-2026. The RBI’s “defense of the rupee” was triggered by a “perfect storm” of global and domestic factors that threatened macro-stability.

Why These Measures Were Necessary?

To curb volatility, the RBI has deployed a combination of direct market intervention and new regulatory “speed bumps.” The RBI maintains that it does not target a specific level for the INR (e.g., it isn’t “defending 95”). Instead, it intervenes to ensure that the movement is gradual and orderly.

Summary of the Recent Measures Taken by the RBI

*Note: Previously, banks could hold “open” positions (which is the difference between their dollar assets and liabilities).

FII flows, INR instability and the Global Capital Nexus

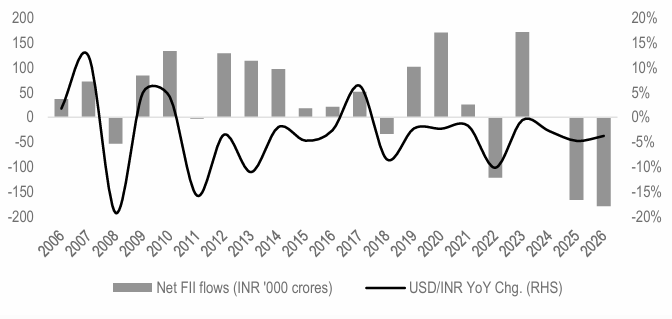

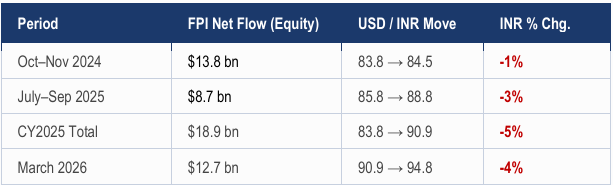

Currency instability is not merely a macro-economic inconvenience, it is a primary deterrent for foreign institutional investors (FIIs/FPIs) allocating to Indian equities and debt. The data tell a clear story – episodes of sharp INR depreciation closely track peak periods of foreign capital outflows, creating a self-reinforcing cycle that policymakers are working hard to break.

Figure 4: Annual FPI Net Flows (INR ‘000 crores) vs. USD/INR (YoY Chg.)

Source: Bloomberg, NSDL, HDFC TRU. Note: Priced as of 15th April 2026.

The Correlation Is Stark

In March 2026, FPIs pulled a record ₹117,775 cr (~$12.7 billion) from Indian equities in a single month, the largest monthly withdrawal ever recorded, triggering a sharp move in USD/INR (down 4% m/m) . By end CY2025, cumulative FPI equity outflows reached $18.9 billion. Through this period, the rupee fell from ₹85 to around ₹90, reinforcing the very uncertainty that was driving outflows in the first place.

Source: Bloomberg, NSDL, HDFC TRU.

Our View: Stability Is the Prerequisite

The INR’s trajectory over the past 15 months encapsulates the challenge facing India’s policymakers at the intersection of domestic growth ambitions and global capital markets. The currency has moved from being overvalued (REER ~108) to undervalued (REER ~94), a rare and potentially significant reversal that, if sustained, could reignite export competitiveness and attract value-driven capital.

The RBI has deployed its toolkit with increasing sophistication – direct intervention, NDF reforms, forward book management, and a calibrated monetary stance. The Apr-26 NDF market crackdown marks a qualitative step-up in willingness to constrain offshore speculation, even at the cost of some market liquidity.

However, the fundamental equation for FII re-engagement is clear; currency stability or at least predictability, must be restored before large-scale foreign capital returns to Indian equity and debt markets. The data confirms that INR volatility and FPI outflows are two sides of the same coin. Breaking this cycle is not just a monetary policy priority, it is essential for India’s ambition to deepen its role in global capital markets and sustain its growth trajectory.

2024 HDFC TRU

2024 HDFC TRU