RBI’s Monetary Policy Review

On Jun 05, 2026, RBI’s Monetary Policy Committee (MPC) took following policy decisions:

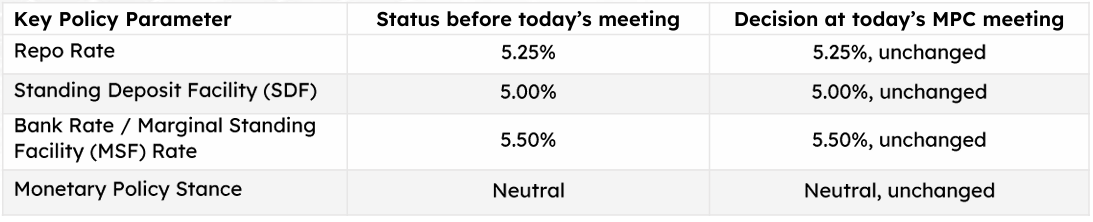

The RBI’s MPC voted unanimously to keep the repo rate unchanged at 5.25%. The MPC also decided to continue with the neutral monetary policy stance.

Executive summary of RBI’s press releases/ press conference:

Global Economy:

- Global economic outlook remains uncertain due to ongoing geopolitical tensions in West Asia.

- Rising energy prices and supply chain disruptions are slowing down economic activity.

- Central banks are facing tough trade-offs, making monetary policy more cautious.

- Major advanced economies are shifting towards tighter monetary policy.

- Equity markets remain strong, driven by optimism around AI growth.

- Bond markets are weak due to concerns about inflation and debt sustainability.

- Risk-averse sentiment and demand for safe-haven assets are increasing.

- Forex markets are volatile, with many emerging market currencies weakening.

Domestic Growth:

- Domestic economic activity has remained stable despite global conflict.

- Manufacturing and services sectors continue to show resilience, with positive business outlook.

- Rising energy and input costs, along with supply disruptions, may slow economic activity ahead.

- Below-normal monsoon may affect agriculture and rural demand.

- Services sector growth, GST changes, and stable employment should support urban consumption.

- Government capital expenditure is expected to remain strong.

- Government measures (MSME support, export promotion, boosting domestic energy production, import diversification) will help manage external shocks.

- Real GDP growth for FY27 is projected at 6.6%, 30 bps lower than 6.9% estimated in Apr 2026 MPC.

Domestic Inflation:

- Crude oil prices for FY27 are expected to be higher at $95/bbl vs. earlier estimate of $85/bbl.

- Higher energy and input costs led to a sharp increase in WPI inflation in April 2026.

- Partial pass-through of higher global crude prices to domestic fuel prices began in May 2026.

- Prices of inputs like LPG, raw materials, chemicals, metals, rubber, and plastics have increased.

- These rising input costs are likely to push CPI inflation higher as firms pass on costs.

- CPI inflation for FY27 is projected at 5.1%, 50 bps higher than 4.6% estimated in Apr 2026 MPC.

- Core inflation (ex-food and fuel) for FY27 is projected at 4.7% vs. 4.4% estimated earlier.

- Upside risks to inflation include – global supply chain disruptions, commodity price shocks, uncertainty in monsoon distribution, potential El Niño conditions.

Other Key Policy Measures:

Key Measures announced to attract foreign capital into the economy:

- Government Securities (G-Secs): Expanded ‘specified securities’ under FAR (Fully Accessible Route) to include 15, 30, and 40-year bonds. Removed limits on short-term investment, concentration, and individual securities for FPIs under the General Route. Combined with tax benefits provided to FPIs by government, these steps aim to boost foreign investment in government borrowing.

- Equity Investments: Increased investment limits for NRIs and OCIs (Overseas Citizen of India) in listed equities without SEBI registration. Extended the same facility to all individual Persons Resident Outside India (PROIs).

- A concessional forex swap facility for External Commercial Borrowings (ECBs) by PSUs and support for banks to bear full hedging costs on 3–5-year FCNR(B) deposits have been introduced to boost foreign currency inflows, with both facilities available until 30th Sep 2026.

Fixed Income Outlook:

- The RBI did not use interest rates to support the currency and kept the policy rate and stance unchanged, as expected.

- We expect RBI to keep rates unchanged in the August policy, with a 50-bps rate hike likely in FY27, possibly starting from the October policy.

- The RBI and government took coordinated steps to boost capital inflows through both short-term measures and long-term structural reforms.

- While the exact impact of these measures is difficult to quantify at this stage, capital inflows could be around $40–50 bn, with potential for higher inflows if global conditions stabilize.

- The Indian rupee is expected to appreciate in the near term, with the USD/INR likely to move towards 93 as capital flows gradually increase.

- Liquidity conditions are expected to remain comfortable in the coming quarter, supported by capital inflows, potential RBI sterilization, and reduced pressure on the rupee.

2024 HDFC TRU

2024 HDFC TRU