FY27 Budget: Key Highlights and Market Impact

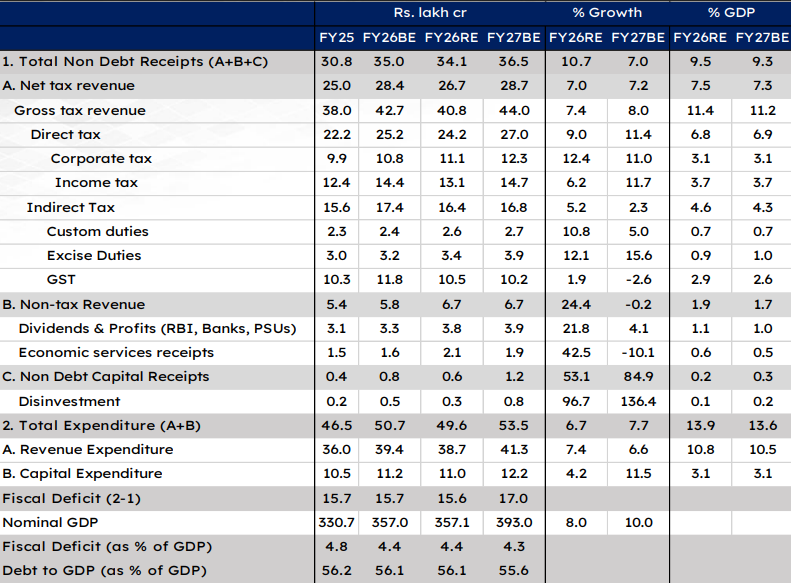

FY27 Union Budget: Key Figures and Fiscal Assumptions

Source: Budget Note, BE – Budgeted Estimates, RE – Revised Estimates

Note: FY27BE figures are based on FY26RE

Growth and Macro Assumptions

- The FY27 Union Budget assumes 10% nominal GDP growth, compared to 8% in FY26 RE. We believe this growth assumption is conservative.

- In absolute terms, nominal GDP is projected at INR 393 lakh crore (USD 4.3 tn, based on a USD/INR exchange rate of 92).

Fiscal Deficit and Debt Position

- The fiscal deficit target for FY27 is set at 4.3% of GDP, marginally lower than 4.4% in FY26.

- In absolute terms, the FY27 fiscal deficit is budgeted at INR 17.0 lakh crore, implying an 8.8% increase over FY26 RE.

- The budget targets a reduction in the debt-to-GDP ratio from 56.1% in FY26 to 55.6% in FY27. This represents a slower pace of consolidation than market expectations.

- The government targets a debt-to-GDP ratio of 49-51% by FY31, indicating that faster consolidation will be required in later years.

Revenue Receipts

- Total non-debt receipts in FY27 are budgeted at INR 36.5 lakh crore, a 7% growth over FY26 RE.

- Gross tax revenue is estimated to grow by 8.0% over FY26 RE, which is considered conservative.

- Lower tax growth is driven by weak indirect tax collections, mainly due to GST rate cuts and lower growth in customs duties.

- Direct tax collections are assumed to grow by 11.4% in FY27. Indirect tax collections are expected to grow by only 2.3%.

- Gross tax buoyancy is projected to decline to 0.8 in FY27 from 0.9 in FY26, largely due to lower buoyancy in indirect taxes following GST cuts.

- Non-tax revenues are expected to remain largely flat at INR 6.7 lakh crore.

- The RBI dividend transfer is estimated at around INR 2.7-2.9 lakh crore, broadly in line with or slightly higher than FY26.

Expenditure and Capital Spending

- Total expenditure in FY27 is budgeted at INR 53.5 lakh crore, reflecting a 7.7% growth over FY26.

- Revenue expenditure is expected to grow by 6.6%. Capital expenditure (capex) is budgeted to grow by 11.5%.

- Capex is budgeted at INR 12.2 lakh crore in FY27. Including government grants, effective capex is estimated at INR 17.1 lakh crore. This implies a 22.1% growth in effective capex over FY26 RE.

Market Borrowings

- To finance the fiscal deficit, the government plans gross market borrowings of INR 17.2 lakh crore in FY27. This is higher than market expectations of INR 16-16.5 lakh crore.

- Net market borrowings (adjusted for redemptions) are budgeted at INR 11.7 lakh crore.

- Net market borrowings including T‑bills are estimated at INR 13.0 lakh crore.

Impact on Fixed Income Market

- We expect elevated gross market borrowings of INR 17.2 lakh crore as the key overhang for the bond market, especially with SDL supply already high in Q4 FY26.

- The sharp rise in net market borrowings (incl. T‑bills) to 76.9% of the fiscal deficit in FY27 BE (from 66.8% in FY26 RE and 58.1% in FY25) is supply‑negative, though stronger‑than‑assumed small savings or other financing sources could partially offset this pressure.

- In the near term, we expect 10‑year G‑sec yield to move up by 5-10 bps, with yields likely to trade in the 6.70–6.80% range.

- We believe market direction will remain data and supply‑driven until there is clarity on the government’s borrowing profile, expected with the H1 FY27 G‑sec borrowing calendar around end‑March 2026.

- Given the volatile, supply‑heavy environment, we remain cautious on high‑duration exposure and continue to prefer accrual‑led strategies. AAA‑rated medium‑duration corporate bonds offer attractive spreads and healthy accruals and remain our focused segment.

Capital Markets – Key Takeaways from Union Budget

- Speculative Derivatives Trading Discouraged: STT on derivatives increased — futures to 0.05% (from 0.02%), options to 0.15%(sell‑side premium from 0.10%, buyer‑side exercise from 0.125%), while cash‑market STT remains unchanged, the move aligns SEBI data showing ~90% of retail F&O traders lose ~₹1 lakh+ annually, signalling intent to curb excessive speculation.

- STT Impact on Arbitrage, Equity Savings & SIF Strategies: The STT hike on futures is expected to create a headline drag of ~20–40 bps for arbitrage funds, ~5–15 bps for equity savings funds, and ~5–20 bps for derivatives‑heavy SIFs, as per industry estimates; however, most of the arbitrage impact is expected to be passed on to long futures participants over time, keeping the steady‑state return impact materially lower than the theoretical maximum.

- Sovereign Gold Bond (SGB) Tax Benefit Restricted: Tax‑free maturity gains only for original holders, likely diverting secondary market demand toward Gold ETFs and mutual funds.

- Higher Overseas Investor Limits (PROI / NRI): Individual PROI limit increased from 5% to 10% and aggregate limit from 10% to 24%, supporting higher foreign equity inflows.

- TDS / TCS Rationalisation: Simplified TDS on manpower services and revised TCS on scrap, minerals and overseas tours ease working‑capital pressure for listed firms.

- MAT Simplified and Reduced: MAT converted into a final tax and rate cut to 14%, No new MAT credit from FY27; existing credits usable only under the new regime, capped at 25% of annual tax, improving earnings visibility and nudging regime shift.

- Income Tax Act, 2025 (Effective 1 April 2026): Replaces the 1961 Act with 25–30% fewer sections, clearer capital‑gains definitions, and reduced interpretational ambiguity, lowering the scope for tax disputes.

- Centralised Form 15G / 15H Filing: Single Form 15G/15H submission via depositories reduces excess TDS for investors holding multiple dividend‑paying stocks.

- One‑Time Foreign Asset Disclosure Scheme: 6‑month window to regularise undisclosed foreign assets with tax and penalty, offering full immunity from prosecution.

- Interest Deduction on Leveraged Investments Removed: Deduction of interest (earlier capped at 20% of income) on borrowings for MF or dividend income withdrawn, improving tax neutrality.

Equity Market Outlook and Sectoral Impact

- The Government’s primary goal was on reviving a weak consumption demand in FY26 through tax cuts which led to a slowdown in capex. With consumption demand showing signs of revival post GST cut in Sep-25 the FY27 the Union budget shifted its focus back towards charting a growth-oriented roadmap for “Viksit Bharat.” It unequivocally reflected in the highest-ever effective capex allocation of INR 17.17trn (+22% YoY) while maintaining a fiscal deficit target of 4.3% (-10bps YoY) for FY27BE. The budget prioritized manufacturing growth through special programmes for semiconductors, rare earth metals, biopharma, electronics manufacturing and MSMEs.

- The Union Budget FY27 reflects the government’s undeterred focus on uplifting economy through long term sustainable investments, while adhering to the fiscal glide path. Increased allocation to housing (PMAY), railways, roads, defence and PLI for Auto & Electronics is positive for industrials, EMS, mining, infrastructure, and pharmaceuticals sectors.

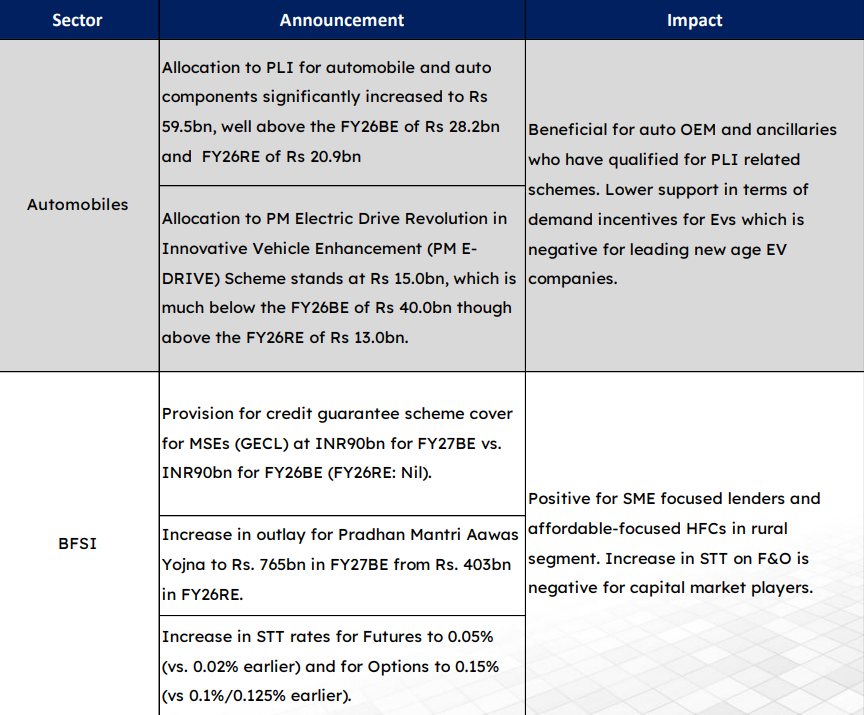

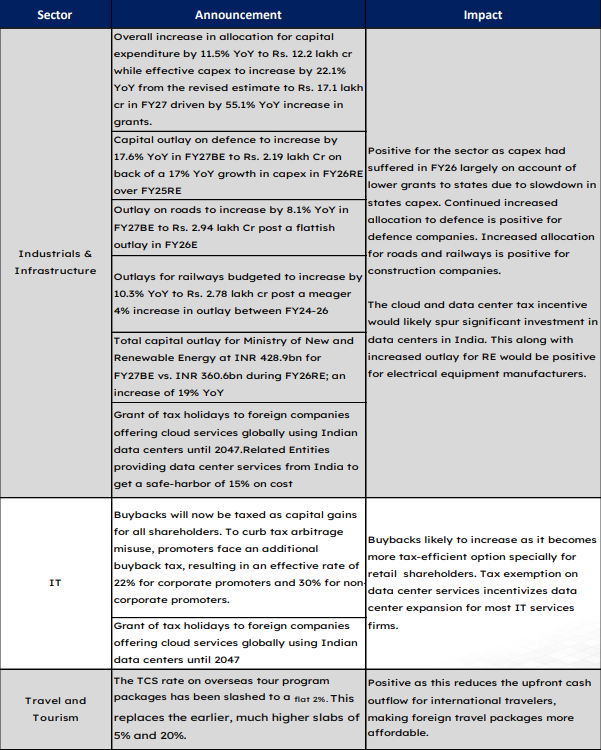

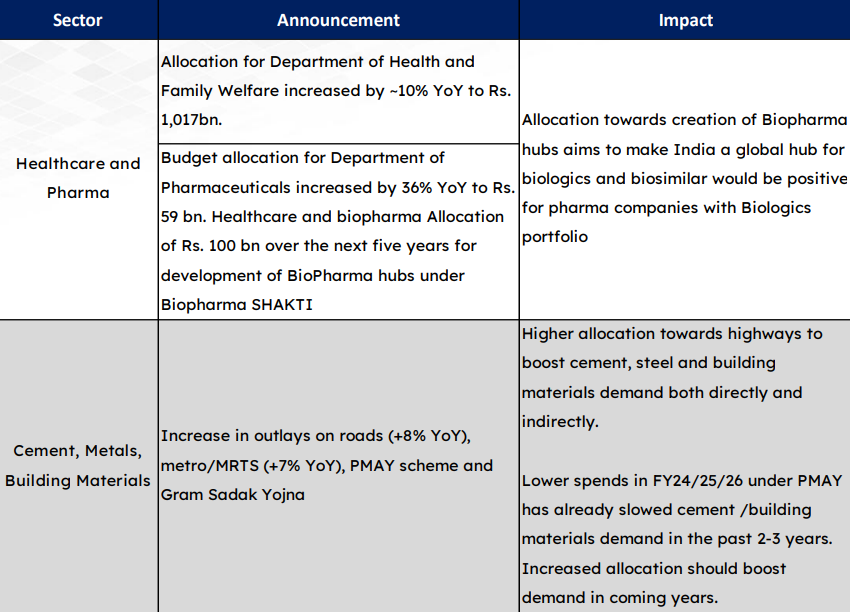

Sectoral Announcements

2024 HDFC TRU

2024 HDFC TRU