The Mechanics of Arbitrage: Spreads, Rates & Market Sentiment

Background

- Arbitrage funds primarily invest >65% of the portfolio in hedged equity positions by simultaneously taking long positions in cash equities and short positions in futures, capitalizing on the cash-future spread.

- The remaining portfolio is allocated to short-term debt instruments, typically in money market securities, which contribute stable income aligned with prevailing interest rates.

- As a result, returns of arbitrage funds are a blend of arbitrage spreads and money market yields, offering a hybrid return profile.

- While debt returns are influenced by short-term yield movements, arbitrage spreads are more dynamic, shaped by multiple market and behavioral factors. This note aims to decode those spread drivers.

Key factors driving arbitrage spreads

|

Factor

|

Rising Arbitrage Spreads |

Falling Arbitrage Spreads

|

| Equity Market Sentiment |

Bullish markets: Strong buying interest leads to futures trading at a higher premium, widening spreads |

Bearish markets: More selling of futures compresses spreads |

| Interest Rates |

Higher rates: Increases cost of carry, widening spreads |

Lower rates: Reduces cost of carry, narrowing spreads |

| FII Hedging/Borrowing Costs |

Higher costs increases spreads |

Lower costs narrows spreads |

| Category Flows |

Lower flows: Fewer arbitrage players, wider spreads |

Higher flows: More participants compress spreads |

| F&O Universe Breadth |

Expansion: More arbitrage opportunities, wider spreads |

Contraction: Fewer opportunities, tighter spreads |

| Market Volatility |

Moderate volatility: Creates pricing inefficiencies and wider spreads |

Low volatility: Efficient pricing narrows spreads |

| Liquidity in Futures Market |

Low liquidity: Increases price impact, widening spreads |

High liquidity: Narrower bid-ask spreads, tighter arbitrage spreads |

Source: Bandhan AMC, Invesco AMC

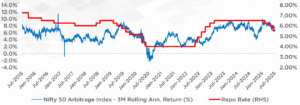

Interest rate cycles are a significant driver of arbitrage spread performance

Source: NSE, RBI, ACE MF

- 3-month annualized rolling return of Nifty 50 Arbitrage Index and repo rate movement has a strong correlation of 0.61 over last 10 years.

- Higher policy rates generally supports higher arbitrage returns. This relationship is primarily driven by the cost of carry component – when interest rates rise, futures tend to trade at a wider premium to spot, enhancing arbitrage spreads.

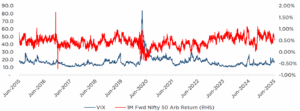

India VIX has negative correlation with Nifty 50 Arb Return

Source: NSE

- A moderate negative correlation of -0.35 between VIX and 1-month forward arbitrage returns likely indicates that excessive volatility or bearish sentiment dampens arbitrage spreads.

- Elevated VIX levels often coincide with risk aversion and unwinding of arbitrage positions, leading to lower or even negative spreads.

2024 HDFC TRU

2024 HDFC TRU