By analysing post‑2020 thematic fund launches, this study examines whether the recent surge in thematic mutual funds has translated into consistent outperformance versus broad‑based indices, or whether returns have largely been driven by short‑term market trends.

Executive Summary

We had earlier published this study titled “Do Thematic NFOs Outperform the Index” in March 2021. In that report, we analysed 62 schemes launched over a 22-year period from 1998 to 2020. Our observations showed that only 44% of the funds outperformed their respective benchmark indices one year after launch, and just 37% of the funds managed to outperform their benchmarks over a three-year period.

We also noted that several thematic funds were launched following strong performance of their respective themes in the period immediately preceding the NFO. However, the outcomes were evenly mixed. Out of 42 such schemes, the respective benchmark indices outperformed 23 schemes.

We finally concluded that funds launched when their underlying themes had outperformed the Sensex prior to the NFO tended to underperform the Sensex post launch, while funds whose underlying themes had underperformed the Sensex before launch generally went on to perform broadly in line with the Sensex.

Post-2020: our Analysis

In this Deep Dive report, we attempt to highlight the recent trends observed in thematic funds, focusing on developments post 2020. For this purpose, we considered all schemes launched from 2020 up to January 2026 as our sample set.

We also seek to understand why thematic funds have emerged as a preferred choice among Retail and HNI investors, and how their performance compares with diversified, broad-based funds. While thematic strategies are available across multiple investment vehicles such as mutual funds, PMSs, and AIFs, our analysis is restricted to thematic mutual funds, as comprehensive and consistent data is most readily available for this category.

Through this report, we have attempted to answer the following questions:

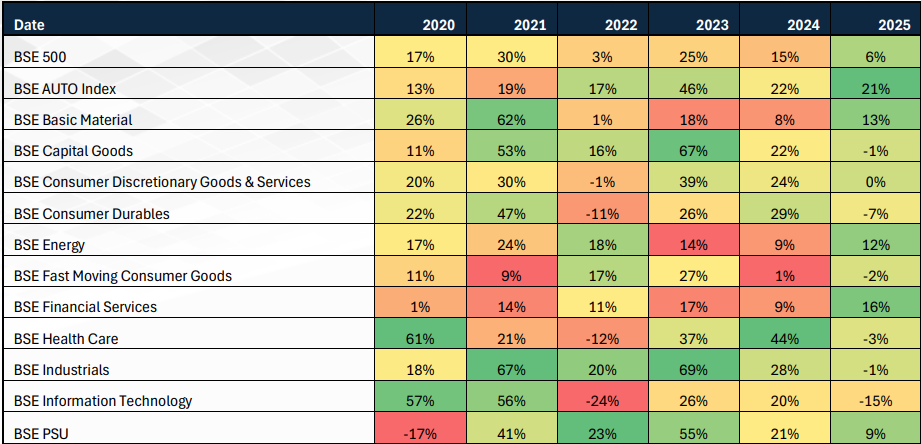

Performance of Sectoral Indices

Thematic funds are among the riskier categories of mutual funds and are therefore suitable only for investors with an aggressive risk profile, given their higher volatility compared to traditional diversified funds. Typically, thematic funds are best positioned as tactical allocations and should act as satellites to an investor’s core portfolio.

One key takeaway from the table is that leadership among themes changes over time; there is no single theme that consistently outperforms every year. Market leadership keeps rotating. For example, BSE Industries and BSE Capital Goods delivered strong outperformance relative to the BSE 500 during the 2020–2024 period. However, this trend has reversed in 2025, with both themes now underperforming the index (‑1% versus a 6% gain for the BSE 500).

Source: ACE MF

Note: i) Calendar year returns provided above; ii) Cell colours signify the highest to lowest returns in that period (green to red).

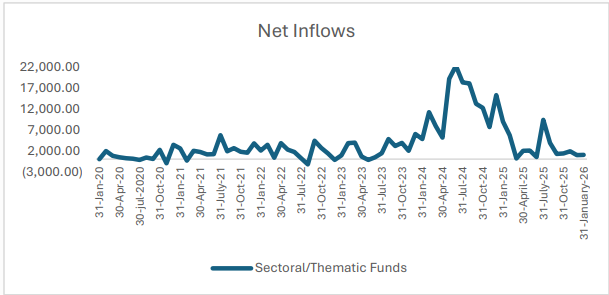

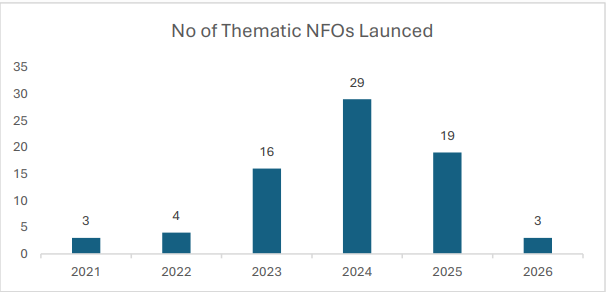

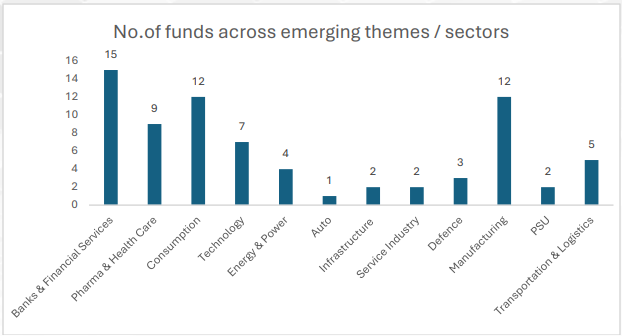

Thematic Mutual Funds: Brief overview, latest trends and key charts:

Source: AMFI Industry Report

Source: ACE MF.

Source: ACE MF.

As seen from the above charts, it is evident that inflows into thematic mutual funds began to pick up meaningfully from 2023, coinciding with a sharp increase in the number of schemes launched. 2024 emerged as the peak year, witnessing both the highest inflows and the maximum number of thematic NFO launches. This momentum moderated in 2025, with a decline in inflows as well as fewer scheme launches.

In terms of theme-wise distribution, Banking & Financial Services, Consumption, Manufacturing, and Pharma & Healthcare have been among the most dominant themes, accounting for a significant share of thematic fund launches during this period.

Question 1: Were the thematic themes launched only because they did great in the immediate period before the launch?

Before the launch of each thematic fund, we compared the performance of the respective theme index over the preceding 12 months with that of a diversified benchmark. For instance, for an IT-themed NFO, we analysed the relative performance of the BSE IT index over the previous year against the BSE 500.

We have excluded the following from our analysis – i) very old funds or those schemes for which the underlying benchmark data was not available, ii) the international equity funds and iii) funds whose underlying benchmark is similar to the as diversified broad-based index, for e.g.; BSE 500 TRI, NIFTY 200 TRI, NIFTY 50 TRI etc.

Based on this screening approach, data was available for 73 thematic funds launched since 2020 with clearly defined benchmark indices. Among these, the benchmark indices of 24 funds had outperformed the BSE 500 TRI on a one‑year return basis prior to launch, while the remaining benchmarks had underperformed the broader index.

While some thematic indices showed recent outperformance before NFO launches, this may not be a reliable indicator, as most funds were launched when the underlying themes were not at their peak. Consequently, the analysis suggests that thematic NFO launches are driven more by fund houses’ conviction in the long‑term growth potential of specific sectors rather than an attempt to capitalize on short‑term sectoral outperformance to attract higher AUMs.

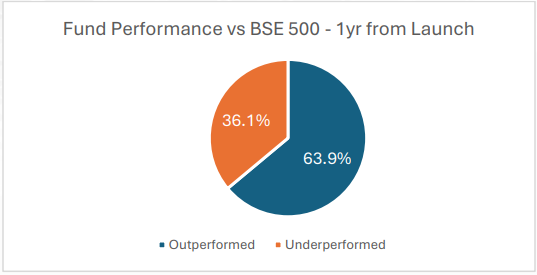

Question 2: Returns performance of the thematic funds vs. the diversified index?

For this analysis, out of a total of 73 schemes, we evaluated the one‑year return performance of 61 thematic funds, as sufficient data was available from their respective launch dates. These returns were compared against the BSE 500 benchmark to assess relative performance.

Source: ACE MF.

In the first year from launch, many thematic funds delivered stronger performance relative to the BSE 500, with 63.9% of the schemes outperforming the benchmark. However, 36.1% of the funds underperformed the index, indicating that while early performance has been favourable for many funds, outcomes have not been uniform across all thematic launches.

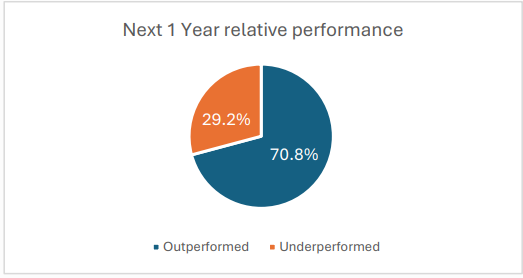

Question 3: What did the past relative performance of the underlying themes (vs. NIFTY) prior to their launch mean for the relative performance of these funds after the launch in the future?

For this study, out of the total of 73 schemes, there were 24 funds whose underlying indices had outperformed the NIFTY 500 during the 12 months preceding the NFO. For the one-year performance analysis, all 24 schemes were considered.

Source: ACE MF.

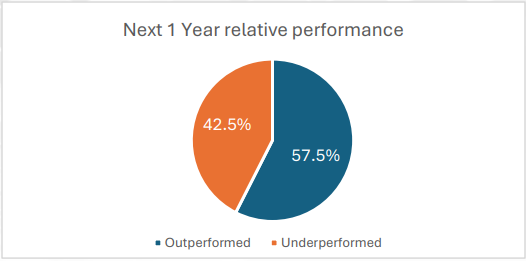

Similarly, we took 39 schemes whose indices underperformed BSE 500 prior to their launch.

Source: ACE MF.

As reflected in the charts above, schemes whose underlying indices had outperformed prior to their launch largely continued to outperform post launch, with around 71% of such schemes beating the index, though not all were able to do so.

Interestingly, even among schemes whose underlying indices had underperformed the BSE 500 before launch, 57.5% of the schemes went on to outperform the index after launch, despite the weaker pre‑launch performance of their respective indices.

Conclusions:

2024 HDFC TRU

2024 HDFC TRU