The need for AIFs in India was boosted with the surge in venture capital investments. The government had been focusing on Venture Capital Funds (VCF) to promote growth of select sectors and early-stage companies. Due to the lack of clarity on the regulatory front, many real estate funds and private equity funds started registering themselves as VCF.

SEBI introduced SEBI AIF regulations in 2012 with an objective to identify distinct investments/asset classes such as Private Equity (PE), Venture Capital (VC), Real Estate (RE), etc.

AIF is an investment avenue to pool in private monies for investing. As per SEBI 2012 regulations, AIFs in India can be incorporated in the form of a trust, company, body corporate, or an LLP.

AIFs can pool monies only on a private placement basis and not from the general public. The monies pooled will be invested according to the defined investment policy stated in the Private Placement Memorandum (PPM).

Just like Mutual Funds, Alternate Investments Funds follow unit accounting, and the underlying securities are held by the AIF and not in the investor’s demat.

Cat I and Cat II AIFs have pass-through taxation. It implies that income/gains generated by these AIFs are not taxed at the fund level, and such income/gains are charged to income tax in the hands of the unit holder in the same manner as if the investments made by the AIFs have been directly made by the unit holder.

For Cat III AIFs, income/gains generated by the AIFs are taxed at the fund level, and net of tax proceeds are passed on to the unit holder/investor.

Taxation on investments in AIFs depends on:

Example:

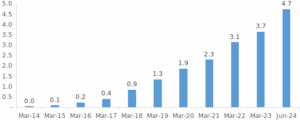

The AIF industry size as of Jun’22 was Rs 6.94 lakh crore. AIFs have witnessed explosive growth over the last few years and have gained popularity amongst sophisticated investors.

Funds Raised by AIFs (Rs lac cr) .

As can be seen in the table above, the funds raised by AIFs have compounded by ~68% over the last 10 years. While the growth has come on a low base, the space has indeed gained traction as AIFs offer access to niche strategies/themes managed by marquee fund managers. Investors’ willingness to take higher risks with unlisted equities and private credits have also bolstered the flows.

PMS is a tailor-made professional investment service offered to HNI investors. PMS are broadly categorized as discretionary and non-discretionary.

In discretionary PMS, the fund manager manages the portfolio as per his/her discretion.

In non-discretionary PMS, the fund manager does all the research which helps/guides an investor to make the decision.

The PMS industry started way before AIFs and had an unstructured beginning with regulatory ambiguity in the 1990s. PMS as an investment vehicle got recognized in the 2000s and gained traction post-2010. Regulatory enhancements, improved transparency, and the advent of technology have helped PMS AUMs grow significantly over the last decade.

When PMS started as an investment vehicle, the minimum investment limit was Rs 25 lacs, which was later increased to Rs 50 lacs in 2019.

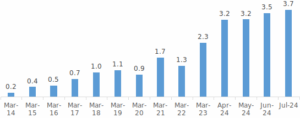

Discretionary Listed Equity PMS AUM (Rs lac cr) .

As can be seen in the table above, the discretionary listed equity PMS AUM has compounded at ~36% over the last decade. We have considered only the discretionary listed equity PMS AUM as typically; this section is most relevant to HNI investing.

| PMS | AIF | |

|---|---|---|

| Pooling & Segregation of Funds | Pooling of investor funds is not allowed. Separate portfolio of every client is to be maintained | Pooling of funds essential in AIFs. Like MFs, unit accounting is done for AIFs too |

| Segregation of Funds | Every client is segregated and kept in different demat accounts | NO segregation is required to be done |

| Minimum Investment | Rs 50 lacs | Rs 1 crore |

| Lock-in Period | No hard lock-in period. Exit load as applicable | Close-ended funds can have prescribed lock-in period |

| Tenure | No minimum tenure. | Minimum 3 years for Category I & II |

| Number of Investors | No minimum / maximum investors | Maximum 1,000 investors per fund. 49 for angel funds |

| Use of Leverage | Not allowed | Category III AIFs can have maximum gross exposure of 200% |

| Documentation | No. of forms for Trading, Demat, & Bank Account | Single Form along with the PPM |

2024 HDFC TRU

2024 HDFC TRU